What Successful Founders Do Differently: Productivity Lessons From US Business Survival Data

There is a comfortable myth in founder culture that the businesses that make it are the ones whose founders worked hardest. Grind more, sleep less, out-hustle everyone, and you win. It is a satisfying story because it puts the outcome entirely in your hands. It is also mostly wrong, and the data on why US businesses actually fail makes that clear.

The failed founders were not, by and large, lazy. Most of them worked brutally hard. They poured years and savings and sleepless nights into their companies, and the companies died anyway. When you look at what actually kills businesses, the pattern is not insufficient effort. It is effort pointed in the wrong direction. The founders who survive are not necessarily working more than the ones who fail. They are working on different things, and they relate to their time, their focus, and their own judgment differently.

So this is not another article about productivity hacks for founders. It is a look at the specific differences in how surviving founders spend their finite attention, set against the hard data on why most businesses do not make it. Productivity, at the founder level, turns out to be far less about doing more and far more about doing the right things, catching problems early, and staying in the game long enough to win. Here is what the survivors do differently, point by point.

First, the stakes: most businesses do not make it

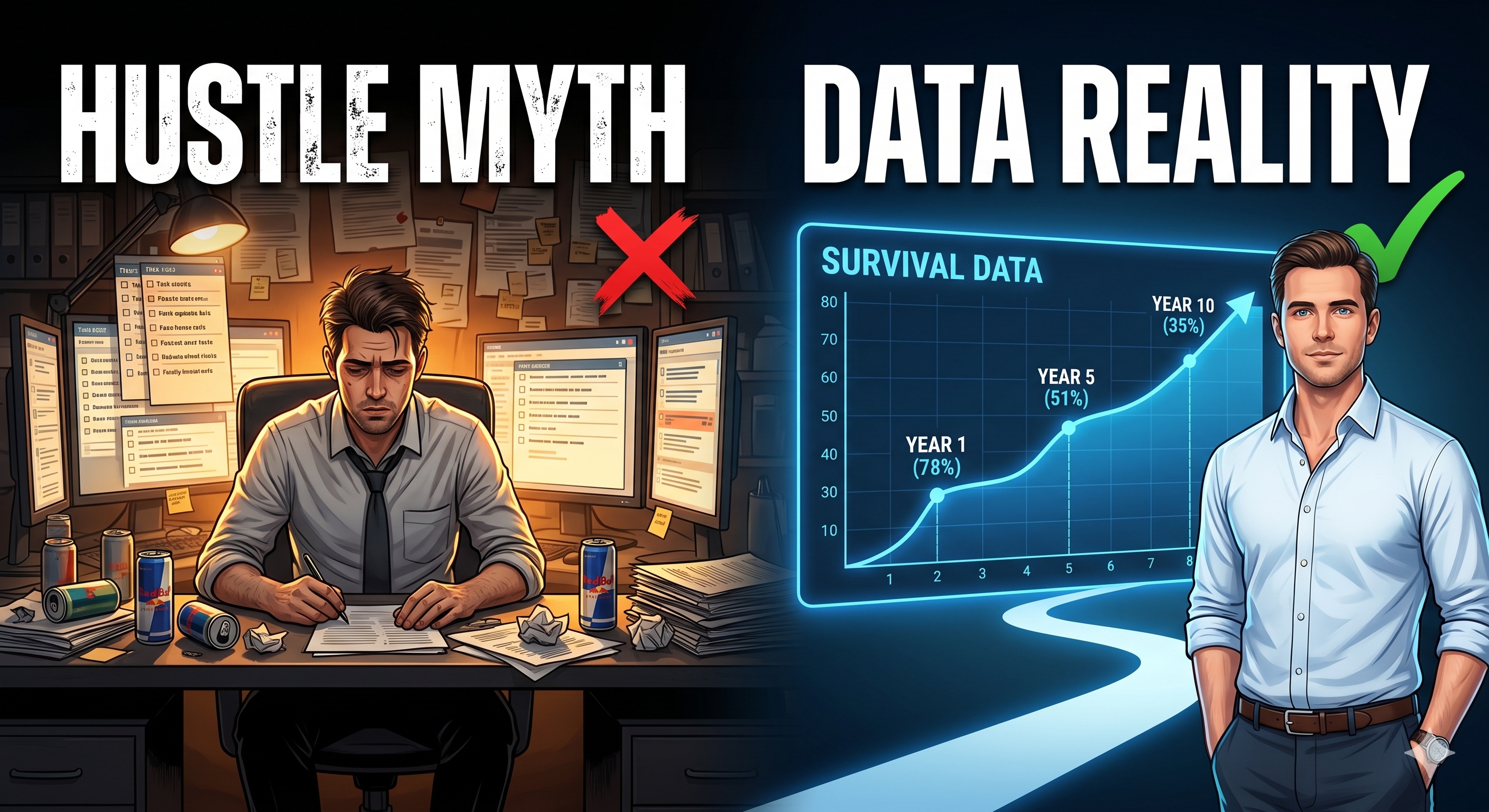

It helps to start with how steep the odds really are, because it reframes what success even means. Based on the most recent US Bureau of Labor Statistics Business Employment Dynamics data, about 22.1% of new US businesses fail within their first year, 48.6% fail by the five-year mark, and 65.3% are gone within ten years.

The scale of this is easy to underestimate. Of the nearly one million new businesses in the latest data, roughly 218,861 closed within their first year, which works out to about 600 a day. Surviving is not the default. It is the exception, and the exception gets rarer the longer the clock runs. Making it to ten years means outlasting roughly two-thirds of everyone who started alongside you.

That backdrop changes how you should read everything that follows. The goal is not to be brilliant. It is to avoid being one of the two in three that do not last, and the founders who manage it tend to share a set of habits that have very little to do with raw effort.

Why businesses actually fail (the honest foundation)

Before contrasting what survivors do, it is worth being precise about what kills the rest, because the real causes are not what hustle culture implies. The most widely cited analysis of startup post-mortems, from CB Insights, found that the single most common reason founders gave for failure was no market need, at around 42%, followed by running out of cash, not having the right team, and getting outcompeted.

The cash point deserves a closer look, because it is the most misunderstood. In CB Insights' more recent analysis of hundreds of failed venture-backed companies, running out of capital showed up in about 70% of failures, but they explicitly call it the final cause of death rather than the root problem, with poor product-market fit (43%), bad timing (29%), and unsustainable unit economics (19%) revealing why the money dried up in the first place. Running out of money is the mechanism. Building something not enough people wanted is usually the disease.

This is the foundation for everything else. The data does not say businesses fail because founders did not work hard enough. It says they fail because they built the wrong thing, misjudged the market, ran the finances into the ground, or could not see the wall coming. Every one of those is a question of where a founder aimed their time and attention. That is what makes this a productivity story, just not the kind the hustle myth tells.

1. They validate before they build

The clearest dividing line is what founders do with their earliest, most precious hours. The ones who fail tend to spend those hours building. The ones who survive spend them finding out whether anyone wants what they are about to build.

This maps directly onto the data. If roughly 42% of failures come down to no market need, updated in more recent analysis to about 43% citing poor product-market fit, then the most expensive mistake a founder can make is pouring effort into a product before confirming the demand. And it is a productivity failure in the truest sense. Months of disciplined, focused, hard work building something nobody needs is worse than doing nothing, because it costs you the runway and the time you cannot get back.

Surviving founders treat validation as the first job, not a step they will get to later. They talk to real potential customers before writing much code. They look for evidence that the problem is painful enough that people will pay to solve it. They are willing to hear that the idea is wrong while it is still cheap to change. Failed founders far more often fall in love with the solution first, build in relative isolation, and only discover at launch that the market is indifferent. The work was real. It was just aimed at a target that was never there. Pointing your effort at a validated problem is the highest-leverage productivity decision a founder ever makes.

2. They treat runway as a live number, not a surprise

Survivors have a different relationship with cash. They know, at any given moment, roughly how many months they have left, and they make decisions against that clock. Founders who fail tend to discover the cash problem only when it is already a crisis.

The numbers around this are stark. One widely cited US Bank study found that about 82% of small businesses fail due to cash flow problems, and in the venture world, the median time from a startup's last fundraise to its shutdown is about 22 months. Money is finite and the clock is always running, whether or not the founder is paying attention.

The productivity angle here is about which numbers you keep in front of you. Surviving founders make runway a metric they watch the way they watch sales, because it sets the deadline for everything else. It tells them how fast they need to learn, how aggressively they can spend, and when they need to either reach profitability or raise again. Failed founders more often keep their heads down in the product and the day-to-day, treating finances as something to deal with later, and later arrives as an emergency with no time left to respond. Knowing your runway is not accounting busywork. It is the single piece of information that determines how much time you actually have to get everything else right.

3. They read the warning signs instead of ignoring them

Businesses rarely die suddenly. They decline, often visibly, for a long time before the end, and the difference between survivors and casualties is frequently just whether the founder was willing to see it. CB Insights found that among failed companies with full data, about 72% saw their health scores decline in the year before shutdown, with an average drop of around 15%, meaning failure was not sudden but a pattern that accumulated.

That finding is quietly damning, because it means the information was usually available. The retention was slipping, the growth was stalling, the unit economics were not working, and in most cases the signals were there to be read months in advance. The founders who survive catch those patterns and act on them while there is still runway to change course. The founders who fail tend to explain the signals away, because they are emotionally committed to the idea and a declining metric feels like a personal verdict rather than data.

This is a productivity issue dressed as an emotional one. Effective founders build the habit of looking honestly at the numbers that matter and responding fast when they turn bad, even when the response means admitting something is not working. Ineffective founders spend their energy defending the original plan against reality. Reality wins either way. The only question is whether you adjust while you still have time, and that depends entirely on whether you are willing to look.

4. They stay ruthlessly focused, and resist scaling too early

Survivors tend to do one thing well before they do many things. Founders who fail are far more likely to chase several opportunities at once, or to scale aggressively before the core business has proven itself. The data on the second mistake is striking: according to research drawn on by Harvard Business Review and the Startup Genome project, about 74% of high-growth startups fail due to premature scaling.

Premature scaling is a productivity failure that looks like ambition. The founder hires ahead of demand, spends on growth before the product retains users, and expands into new markets before dominating the first one. It feels like progress because there is so much activity. But it burns the runway faster while the underlying business is still unproven, which turns a fixable problem into a fatal one.

The founders who last are disciplined about sequence. They concentrate their effort on making the core thing genuinely work, with real customers who stay, before they pour fuel on it. They say no to opportunities that would split their focus, even attractive ones, because they understand that a startup's scarcest resource is attention and spreading it thin is how you end up mediocre at everything. Focus is not a personality trait here. It is a deliberate productivity strategy, the choice to go deep on what matters rather than wide on what tempts you, and it is one of the most reliable markers of the businesses that survive.

5. They make fast, reversible decisions instead of stalling on perfection

Speed of learning is a survival trait, and it comes down to how founders make decisions. The ones who last tend to decide quickly on anything reversible, ship, watch what happens, and adjust. The ones who fail more often stall, deliberating and polishing in search of a perfect answer that the market alone can provide.

This matters because of timing. With bad timing cited in roughly 29% of startup failures, the speed at which you find product-market fit is often the difference between catching a market as it opens and arriving after the window has closed. Every week spent perfecting something untested is a week not spent learning whether it works.

The productivity logic is about matching the speed of the decision to its reversibility. Surviving founders make small, reversible bets fast, because the cost of being wrong is low and the information you gain is high. They reserve slow, careful deliberation for the rare decisions that genuinely cannot be undone. Failed founders often invert this, agonizing over reversible choices while real time and runway drain away, treating every decision as if it were permanent. The validation cost of testing an assumption is usually measured in days. The cost of discovering the assumption was wrong after a year of building is measured in years of your life. Founders who move fast on the cheap experiments simply learn more per month than founders who wait, and in a race against a finite runway, learning rate is everything.

6. They work on the business, not just in it

There is a trap that catches an enormous number of founders: they get so consumed by the daily operations that they never step back to steer. Survivors protect time to work on the business, the strategy, the priorities, the direction. The ones who fail get swallowed by working in it, doing the urgent tasks until there is no room left to think about whether they are even pointed the right way.

This connects to the deeper failure pattern. When 42% of businesses fail from a lack of market need, a real contributor is that the founder was too buried in execution to notice the market was not responding. You cannot course-correct a direction you never make time to evaluate. The operational treadmill feels productive because you are always busy, but busyness inside a doomed direction is not progress.

The founders who last build in deliberate time to lift their heads, usually on a regular rhythm, and ask the questions that operations crowd out. Is this still working. Where is the evidence. What should we stop doing. They treat that strategic time as non-negotiable, because they understand it is the highest-leverage work they do, even though it produces nothing visible in the moment. Founders who fail tend to let the urgent permanently crowd out the important, mistaking motion for direction. Carving out time to think is not indulgent. For a founder it is the work that decides whether all the other work was aimed correctly.

7. They build the right team and actually delegate

No founder survives alone past a certain point, and how they handle people is a clear divider. With not having the right team cited in roughly 23% of startup failures, the team question is a top-tier killer in its own right. Survivors get two things right that failures get wrong: they hire for their own gaps, and they let go of the work that others should own.

The productivity logic is about leverage. A founder's time has a ceiling, and the only way past it is other people doing work the founder no longer has to. Surviving founders identify the skills they lack and bring in people who have them, rather than surrounding themselves with people just like themselves. Then they delegate genuinely, handing over real ownership so their own time frees up for the decisions only they can make. Failed founders more often either try to do everything themselves, becoming the bottleneck that caps the whole company's speed, or they hire poorly under pressure and end up with a team that cannot execute.

This is one of the hardest shifts for founders, because the same intensity and control that helped at the start becomes a liability at scale. The ones who survive recognize that their job changes from doing the work to building the system and the team that do the work. Refusing to make that shift, out of perfectionism or an inability to trust, keeps a company stuck at the size of one exhausted person, which is rarely big enough to survive.

8. They manage their own energy for a long game

The final difference is the most personal, and the most overlooked. Survival is a multi-year endurance test, and given that only about a third of businesses are still standing after ten years, the founder's own sustainability is part of the equation. Survivors tend to manage their energy for the long haul. Many who fail burn themselves out and start making bad decisions from a depleted, reactive state.

This is where the hustle myth does real damage, because it glorifies exactly the behavior that breaks founders. The founder is the company's most important decision-making instrument, and a chronically exhausted, sleep-deprived, burned-out founder makes worse calls, reads signals less clearly, and reacts emotionally where calm judgment was needed. Given how much of survival comes down to seeing problems early and deciding well under pressure, a degraded founder is a direct threat to the business, not a badge of commitment.

The founders who last treat their own clarity and stamina as resources to protect, not prove. They sleep enough to think straight. They avoid the kind of total burnout that ends in either a health collapse or a panicked, terminal decision. They pace themselves for a journey measured in years rather than sprinting until they break. This is the productivity insight that ties all the others together: every good decision in this article depends on a founder clear-headed enough to make it, and you cannot make clear-headed decisions for years on end while running yourself into the ground. Sustainability is not the opposite of ambition. Over a ten-year survival horizon, it is what ambition requires.

What it actually adds up to

Read these differences together and a single theme runs through all of them. The founders who survive are not winning on effort. They are winning on direction. They aim their work at validated problems, watch the numbers that set their deadline, catch trouble early, concentrate their focus, learn fast, make time to steer, build leverage through people, and stay clear-headed enough to keep doing all of it for years. None of that is about working more hours. It is about where the hours go.

That reframes productivity for a founder entirely. The question is not how do I do more. It is am I doing the things that actually determine survival, or am I busy inside a direction that the data already predicts will fail. Hard work aimed at the wrong target is the most common story in the failure statistics, and it is precisely the story that hustle culture cannot see, because it measures effort instead of direction.

It is worth being honest about the limits of all this. Productivity and focus are necessary, but they are not sufficient. Plenty of disciplined, focused, clear-headed founders still fail because of timing they could not control, capital they could not raise, a market that shifted, or simple bad luck. The data is full of well-run companies that died for reasons outside any founder's control. Doing these things does not guarantee survival. But not doing them is a reliable way to end up in the two-thirds that do not last. You cannot control whether you win. You can control whether you are pointed at the right things while you try, and that, far more than how hard you grind, is what separates the founders still standing from the ones who are not.

Takeaways

Most US businesses fail, with roughly 22% gone in the first year, about half by five years, and 65% by ten years. The failures are rarely about a lack of effort.

The real causes are about direction. The most cited reasons for failure are no market need, running out of cash, the wrong team, and bad timing, which means founder productivity is about doing the right things, not doing more things.

Surviving founders share a pattern: they validate before they build, treat runway as a live number, read warning signs early, stay ruthlessly focused and avoid premature scaling, make fast reversible decisions, protect time to work on the business, build the right team and delegate, and manage their own energy for a multi-year game.

The unifying lesson is that direction beats volume. Hard work aimed at the wrong target is the most common failure story there is. Productivity for a founder means aiming effort at what actually determines survival.

The honest caveat is that focus is necessary but not sufficient. Timing, capital, market shifts, and luck all matter and lie partly outside a founder's control. Doing these things does not guarantee success, but failing to do them reliably leads to the majority outcome, which is closure.

FAQ

What percentage of US businesses fail?

Based on the most recent US Bureau of Labor Statistics data, about 22% of new US businesses fail within their first year, roughly 49% fail within five years, and about 65% are no longer operating after ten years. Surviving past a decade means outlasting close to two-thirds of the businesses that started at the same time, which is why long-term survival is treated as a genuine achievement rather than the norm.

What is the number one reason businesses fail?

The most cited reason in analyses of startup post-mortems is a lack of market need, accounting for around 42% of failures, more recently framed as poor product-market fit at about 43%. While running out of cash appears in a large share of failures, it is usually the final symptom rather than the root cause. Most companies that run out of money do so because not enough people wanted what they built.

Do successful founders just work harder than founders who fail?

The data suggests not. Most failed founders worked extremely hard, and effort is rarely what separates survivors from casualties. The difference is direction. Founders who survive aim their work at validated problems, watch the right numbers, focus deeply rather than spreading thin, and adjust quickly when signals turn bad. The lesson is that doing the right things matters far more than simply doing more.

What does it mean to validate a business idea before building it?

It means confirming that a real, paying demand exists before investing significant time and money in building the product. In practice this looks like talking to potential customers, testing whether the problem is painful enough that people will pay to solve it, and looking for evidence of genuine pull from the market. Since around 42% of failures stem from building something nobody needed, validation is one of the highest-leverage things a founder can do early.

Why is premature scaling so dangerous for startups?

Research associated with Harvard Business Review and the Startup Genome project found that roughly 74% of high-growth startups fail due to premature scaling. Scaling too early means hiring ahead of demand and spending on growth before the core product has proven it can retain customers. This burns through limited runway while the business is still unproven, turning a fixable problem into a fatal one. Founders who survive tend to make the core work first before pouring fuel on it.

How important is cash flow management for survival?

It is critical. One widely cited study found that about 82% of small businesses fail due to cash flow problems, and money running out appears in roughly 70% of startup failures. Founders who survive tend to know their runway at any moment and make decisions against that clock, because it sets the deadline for everything else. Treating finances as something to handle later often means discovering the problem only when it is already a crisis with no time to respond.

Does good productivity guarantee a business will succeed?

No. Focus and good execution are necessary but not sufficient. Many well-run, disciplined companies still fail because of timing, an inability to raise capital, market shifts, or plain bad luck, all of which lie partly outside a founder's control. Strong productivity habits do not guarantee survival, but neglecting them reliably leads to the majority outcome, which is closure. Founders can control whether they are aimed at the right things, even if they cannot control the result.

Date-based AI Task Manager

Plan smarter, execute faster, achieve more

Create tasks in seconds, generate AI-powered plans, and review progress with intelligent summaries. Perfect for individuals and teams who want to stay organized without complexity.

Get started with your preferred account